Yesterday the Department of Energy,'s EIA released their EIA-914 Monthly Natural Gas Gross Production report. Fist a little background: prior to Jan-05, the EIA had published estimates of natural gas production based on data supplied by or collected from individual State agencies and the Minerals Management Service. Because these production estimates were not considered sufficiently timely nor accurate to meet customer needs the EIA instituted this monthly survey, which collects production data directly from well operators.

This month's 914 report was modestly bullish, showing continental U.S. gas production to be approximately -1.4 bcf per day (a negative number is bad, positive is good for gas prices) out of balance (in from nearly -3.5bcfpd during massive Aug-09 production builds)

However, it is unclear whether the sequential decline is driven by either production shut-ins (operators such as CHK and ECA stated their voluntary shut-in volumes, and it is likely that others followed suit as spot gas prices declined to sub $2/mcfe in early Sep-09, and only gradually improved to ~$3.5/mcfe by the end of the month) or natural declines in production capacity (TPH had estimated 0.5 bcf/day of natural wellhead declines back in late Nov-09).

Net-net, the 914 data seems inconclusive and ~1.5 bcf/day of production shut-ins seems statistically unrealistic based upon historical trends. Additionally, the latent winter weather is not helping to clarify the demand side of the situation - I will be watching the weekly storage data tomorrow morning for implied supply-demand, which will no longer be disguised by full storage effects.

Wednesday, December 2, 2009

Trade Update: "Going for the Gold" - Part II

Well, I left money on the table. What can I say. I exited the directionally long GLD and long GLD Gamma trade a day too early, and missed out on an additional 1.35 of upside today alone.

It is bitter sweet to have closed out of the position. This has been my largest trade to date, on a risk-weighted basis, comprising ~12% of portfolio 20-day VaR / PML - the upper threshold of my internal trading guidelines. Now without another week of sleepless nights, I can re-focus my efforts back to my core strategies.

While I am thrilled with how well the trade worked out already, my naivete reminds me of Lefevre's old adage to follow the path of least resistance; I had been to caught up in the short-term horizon of this trade, that I forgot to acknowledge the influence of the longer-term momentum.

It is bitter sweet to have closed out of the position. This has been my largest trade to date, on a risk-weighted basis, comprising ~12% of portfolio 20-day VaR / PML - the upper threshold of my internal trading guidelines. Now without another week of sleepless nights, I can re-focus my efforts back to my core strategies.

While I still believe there are reasonable fundamentals underlying the demand for Gold, I do believe there is a non-negligible probability of jump risk given that this rally seems to be catalyzed by a crowded USD-carry trade and the potential for a strengthening dollar (Friday's job report will be key). A short squeeze on the Short Dollar-Long Risk trade, as talked about in Mauldin, seems inevitable but not imminent. If the U.S. economy begins to mend itself ahead of schedule, the potential for rate increases will be dollar positive-gold negative; again, the unemployment rate will serve as our barometer for indications of FOMC posturing. Now that I have reduced risk, I am thinking about ways to quantitatively express my fundamental views on this jump risk, particularly in E.M., perhaps via deep OTM puts and long-vol expressions on E.M. ETFs? Brazilian puts (EWZ) or short Chinese Real Estate (TAO) anyone? I also want to re-shift my focus back onto natural gas as we get into the winter draw season. More to come...

Monday, November 30, 2009

Trade Update:"Going for the Gold"

The Wednesday 11/25 rally in Gold caused the Dec 115 GLD Calls (GCZ-LG) to be exited on 3/4 of the positions risk capital (I have established internal +/- 40% option guidelines for 1M ATM options where time to expiry is greater than 20 days and Gamma is between 5-15).

As discussed in a prior post, we have seen a sharp technical pullback catalyzed by the fear of  Dubai's debt dilemmas, which gave way to a pronounced pullback from nearly all risky assets on the 27th. Managers have finally been reminded that the crisis is not over, and that risk premiums exist for a reason. Fortunately, the systematic trading style has been advantageous in uncertain times like these: the flight-to-quality led resulted in a strong appreciation of the dollar and a nice consolidation on the GLD.

Dubai's debt dilemmas, which gave way to a pronounced pullback from nearly all risky assets on the 27th. Managers have finally been reminded that the crisis is not over, and that risk premiums exist for a reason. Fortunately, the systematic trading style has been advantageous in uncertain times like these: the flight-to-quality led resulted in a strong appreciation of the dollar and a nice consolidation on the GLD.

Dubai's debt dilemmas, which gave way to a pronounced pullback from nearly all risky assets on the 27th. Managers have finally been reminded that the crisis is not over, and that risk premiums exist for a reason. Fortunately, the systematic trading style has been advantageous in uncertain times like these: the flight-to-quality led resulted in a strong appreciation of the dollar and a nice consolidation on the GLD.

Dubai's debt dilemmas, which gave way to a pronounced pullback from nearly all risky assets on the 27th. Managers have finally been reminded that the crisis is not over, and that risk premiums exist for a reason. Fortunately, the systematic trading style has been advantageous in uncertain times like these: the flight-to-quality led resulted in a strong appreciation of the dollar and a nice consolidation on the GLD.

I am still looking for directionally net long exposure to GLD. I am rebuilding an entry back into the Dec and Jan ATM calls. However, Skew is still biased to the downside and 5% OTM strangles are still too expensive to capture long-vol, based upon historical volatility cone analysis.

So far, profit on the trade has been 38.8% in 3 days net of transaction costs and with vol of 49%, leading to a Sharpe of 0.79 over the trade's duration.

Tuesday, November 24, 2009

Going for the Gold

The decline in the dollar and the low interest rate environment are clearly affecting asset prices globally. Capital is fleeing the dollar and flowing everywhere else. While gold has certainly been a beneficiary of this technical rally (price chart at right), its rise has been built on reasonable fundamentals and real demand.

While gold may seem to be structurally overbought (perhaps thanks to the margined prop desks and other carry traders?) there may be some near-term opportunities to build a stronger position. The thesis is as follows:

1. Since March, capital flowed out of risk-less and into risky assets

2. Foreign risk takers needed to hedge their USD exposure of these risky investments, thus exacerbating the dollars decline.

3. Risk has become fundamentally under priced in recent weeks (LIBOR-OIS spreads had dropped back down to pre-Lehman levels earlier this month).

4. Now, sentiment is beginning to shift back to fundamentals

5. We may see a technical pull-back with year-end window

dressing ahead

6. Given the lagged nature in changing correlation structure, the GLD-SPY positive correlation may be expected to hold during a short-term market correction. This will be an opportunity to add to a hedged position in Gold (vis-a-vis the GLD) that will benefit from the long-term macro picture in the U.S. and abroad.

Gold has continued to set newer highs in nominal terms with reasonable fundamentals (i.e., there is increasing real, physical demand for the asset).

Price action in the GLD underlying has been roughly in-line with the expectations given by

option prices, but in recent days, the volatility skew is suggesting increased put buying (see volatility analysis at right), which may be indicative of bearish sentiment in advance of a pullback.

Additionally, the CBOE's gold volatility index (GVZ) has been fluctuating between 20-30 since late August, and the spread between 20D HVOL of GLD and 20D lagged IVOL on GLD has not changed meaningfully in the past several weeks.

Most interestingly, since March, Gold has shifted polarity, becoming highly correlated with the S&P500 (SPY). From a ratio perspective, the GLD/SPY ratio is below recent historical highs.

S&P500 (SPY). From a ratio perspective, the GLD/SPY ratio is below recent historical highs.I am keeping my eyes on theATM Dec-09 115 calls (expiring in 25 days), which have pulled back 22.3% since Monday's gap-open on the GLD (GS quote at $2.36). The ratio of 25d IVOL to HVOL is is in from the wides of 1.6x last week, now at 1.38x (21.26% iVol and 15.46% hVol, annualized).

Spend now, pay Later... Indications of weakness in the dollar "Carry Trade"?

The Macro Picture:

While the administration may have signaled that they will get serious about reducing the deficit next year - after a massive health care program is passed - our fiscal situation and economic position continue to deteriorate. Spending has reached nearly 1/4 of GDP (the highest since WWII) amidst some of the largest revenue shortfalls in nearly three decades. The planned deficits, which are expected to reach nearly $17 trillion within the next decade, are believed to lead to not only to crowding out of domestic investment, but also to crowding out of future exports, thus impairing our international competitiveness. It is expected that the publicly held federal debt will double in the next decade from its current 41%, well above the G20 average. As was postulated by Douglas Hotlz-Eakin in the WSJ, "at what point... do rating agencies downgrade the United States?"

However, the current predicament and absence of a clearly articulated, credible plan to reduce the deficit has put extreme relative pressure on the dollar. It has engendered what appears to be one of the greatest carry trades of all time. That trade is showing signs of weakness, and may present some compelling buying opportunities in the near-term.

I don't believe that we will witness a sudden crisis, similar to those experienced by emerging market economies. There simply are no reasonable alternative fiat reserves to the U.S. dollar. As a key beneficiary of the dollar's weakness, gold will perhaps continue to have a renewed importance in countries global reserves in the time ahead.

Over the past several months, capital has progressively flowed from the safe

security of the USD and U.S. treasuries and into a search for yield. We have seen this not only in the impressive performance of emerging economics (and likely bubbles that are emerging from China's financial market to Brazil's Bovespa), but also in our own markets as financials, commodities and energy in particular have made dramatic surges. However, the tide appears to be turning. In the two sector maps at right, you can see how sentiment has become more sober in the past week relative to the

past 45 days.

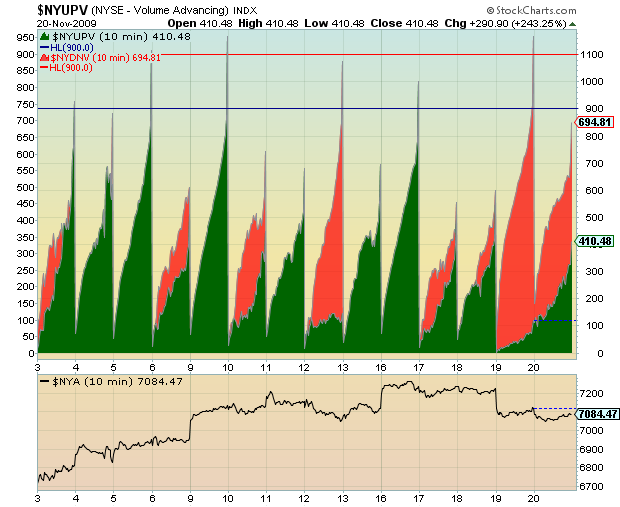

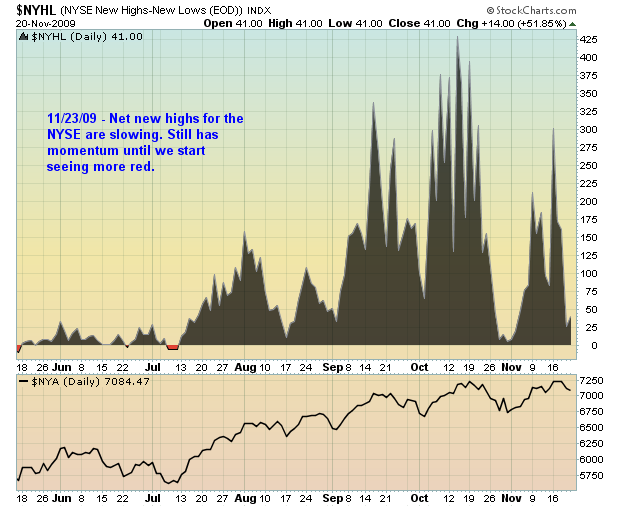

In recent days there have been a number of indicators that would suggest we may be bracing for a re-assessment of risk. T-bills have become negative (great commentary from Lakewood on the implications of this), rallies have been built on decreasing volume over the past month, volumes are rising on decliners and down days, the net number of new highs for the NYSE are slowing, and the S&P is consolidating with resistance at the 1100 level (image at right), amongst many others.

Wednesday, November 11, 2009

Are WTI's days over?

At the end of October, Saudi Aramco announced their decision to abandon the Platt's WTI-based benchmarks in favor of Argus' new sour crude / U.S. gulf coast index, largely out of fears for future capacity limitations at Cushing. This begs the question of how substantial the current and future shift in momentum will be away from WTI-based benchmarks.

I initially believed the short-term effect of this change would likely be minimal, particularly given that there is no real liquid alternative to the NYMEX/CME WTI contract. Additionally, the debate around Cushing as a suitable delivery point has been going on for years.

However, I am beginning to re-evaluate my medium-to-longterm thesis based upon the following recent data points:

(1) Shifts in open interest suggest a subtle trend away from WTI is already underway: there has already been a subtle shift away from trading activity in WTI to Brent this year, as confirmed in the open interest figures.

(2) New ETF instruments will open additional avenues to route capital away from WTI: new news that UNG / USO's parent, the United States Commodity Fund, has announcement a potential launch of an ETF tied to the Argus sour crude index. While this likely won't replace USO, the dramatic growth of USO is a testament that there may be substantial demand for this type of product, and;

(3) New CME futures contract will have the largest impact on liquidity shifting away from WTI: CME's expectation to likely launch new contract at the end of the year to capitalize on the success of the Argus Index. It would be interesting to see the curve dynamics and level of contango that come about under this new contract, as this may not only present some interesting relative value trades with WTI dynamics, but if the contango is more favorable, perhaps we will see a shift out of USO and into the new ETF products.

As crude has been used by investors as less of a physical asset, and more of a global financial asset in recent years, it would seem reasonable that the commodities physical limitations would ultimately lead to natural market frictions. After all, there is only so much storage, and as such, Oklahoma cannot continue to be the best entry point forever.

The Great Accommodation leads to the Great Devaluation?

It was highlighted today that the Dollar now trades at the lowest level to the Euro since October 26th (see charts at right). Specifically, the Dollar's two-week low against the Euro comes in advance of a report due out tomorrow, which is expected to show Europe's economy had expanded last quarter, thereby further dampening demand for the U.S. currency. However, the escalating headwinds are not new, and the Dollar has remained under pressure for several weeks now. Correlations between risky assets and currencies, the dollar in particular, are at notably high levels.

This extreme negative correlation, in the case of the dollar is quite possibly predicated upon, amongst a number of things, a hunger for risky assets by foreigners that leaves them needing to hedge their Dollar exposure. Underlying this trend are the accommodative policy measures taken by major central banks, who will likely continue to provide support to risky assets "for an extended period." This implies sustained Dollar weakness, and certainly while rates remain at historic lows under "stable inflation expectations."

More to the point, increased hedging needs are quite possibly undermining the dollar. Take notice of the increasing correlation between the dollar and risky assets, for which the S&P500 serves as a proxy. As one of the most negatively correlated currencies, at nearly -60% return correlation over the past 60 days, the evidence would seem to indicate that foreign investors with domestic assets may be more heavily currency-hedged than domestic U.S. investors with foreign assets.

While global risk sentiment tends to be more sensitive to rate hikes in major countries, with the Fed and ECB in a holding pattern, it is likely that the non-Major countries will see relative appreciation. Evidence is available in the AUD which recently began raising rates and now trades at 0.9352 per Dollar, up nearly 11% since August 31.

This begs the question, on whether or not central banks' great accommodations in monetary and fiscal policies will lead to the great devaluation of the Dollar?

Subscribe to:

Comments (Atom)

{kind=link}

{kind=link}