While the administration may have signaled that they will get serious about reducing the deficit next year - after a massive health care program is passed - our fiscal situation and economic position continue to deteriorate. Spending has reached nearly 1/4 of GDP (the highest since WWII) amidst some of the largest revenue shortfalls in nearly three decades. The planned deficits, which are expected to reach nearly $17 trillion within the next decade, are believed to lead to not only to crowding out of domestic investment, but also to crowding out of future exports, thus impairing our international competitiveness. It is expected that the publicly held federal debt will double in the next decade from its current 41%, well above the G20 average. As was postulated by Douglas Hotlz-Eakin in the WSJ, "at what point... do rating agencies downgrade the United States?"

However, the current predicament and absence of a clearly articulated, credible plan to reduce the deficit has put extreme relative pressure on the dollar. It has engendered what appears to be one of the greatest carry trades of all time. That trade is showing signs of weakness, and may present some compelling buying opportunities in the near-term.

I don't believe that we will witness a sudden crisis, similar to those experienced by emerging market economies. There simply are no reasonable alternative fiat reserves to the U.S. dollar. As a key beneficiary of the dollar's weakness, gold will perhaps continue to have a renewed importance in countries global reserves in the time ahead.

Over the past several months, capital has progressively flowed from the safe

security of the USD and U.S. treasuries and into a search for yield. We have seen this not only in the impressive performance of emerging economics (and likely bubbles that are emerging from China's financial market to Brazil's Bovespa), but also in our own markets as financials, commodities and energy in particular have made dramatic surges. However, the tide appears to be turning. In the two sector maps at right, you can see how sentiment has become more sober in the past week relative to the

past 45 days.

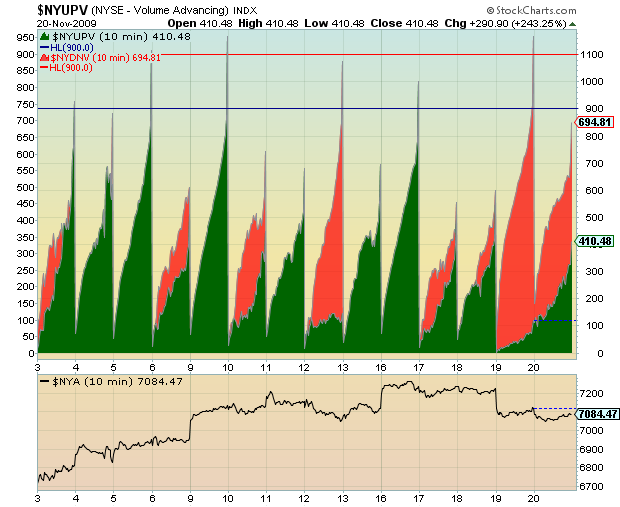

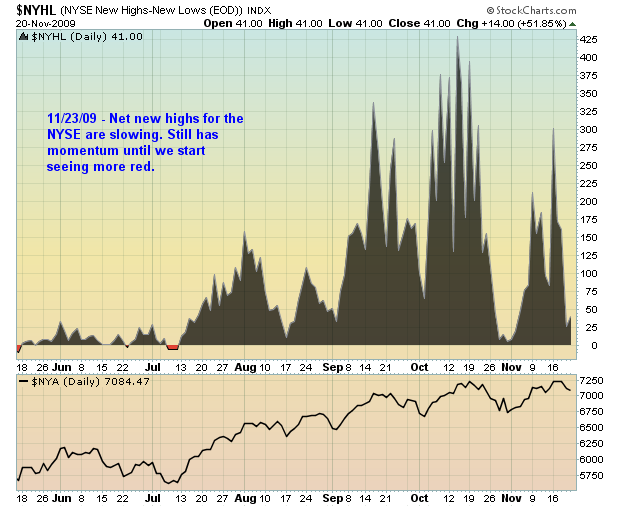

In recent days there have been a number of indicators that would suggest we may be bracing for a re-assessment of risk. T-bills have become negative (great commentary from Lakewood on the implications of this), rallies have been built on decreasing volume over the past month, volumes are rising on decliners and down days, the net number of new highs for the NYSE are slowing, and the S&P is consolidating with resistance at the 1100 level (image at right), amongst many others.

{kind=link}

{kind=link}

No comments:

Post a Comment